|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

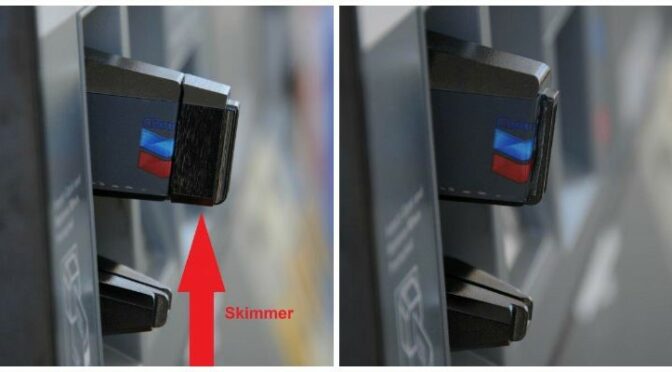

A Fort Scott Police Department case that began last summer at a local gas station is ongoing.

At the Pete’s Convenience Store on East Wall in August 2020, staff noticed that a lock on the pump door had been tampered with.

The store’s maintenance employee called the FSPD immediately.

An investigation was started by retrieving the skimmer and calling other local and nearby towns to tell them of the illegal activity at the gas pump.

Skimmers are illegal card readers attached to payment terminals. These card readers grab data off a credit or debit card’s magnetic stripe without your knowledge, according to https://www.consumer.ftc.gov/blog/2018/08/watch-out-card-skimming-gas-pump Criminals sell the stolen data or use it to buy things online.

FSPD Detective Sargeant Brian Thurston mailed the skimmer to the U.S. Secret Service.

“They have the technology to get information off of the device to try to identify the perpetrator,” he said.

“The device is Blue Tooth,” he said. “The bad guy can come back and get info off of it.”

The FSPD received information back from the Secret Service on Feb. 16, 2021.

Forty-five people had their information on the skimmer, Thurston said. He has made contact with them.

“We don’t believe any info was retrieved by the suspect,” he said.

His next step is to contact the Kansas Bureau of Investigation and get assistance “to identify the device, then attach someone to that device, to identify a suspect,” he said.

Back in August, the FSPD called local gas stations and also area ones, to tell them of the skimmer.

“In Louisburg a skimmer was at an ATM inside of a store,” Thurston said.

Pete’s Convenience Store has since replaced all the locks on the gas pumps.

The 45 people who were listed on the skimmer are being notified to change their credit card, as a safety precaution, he said.

The Secret Service has sent Thurston information on the device that was connected to that skimmer.

The investigation is ongoing, he said.

How to protect oneself from skimming.

“There is a security seal on the door of the gas pump,” Thurston said. “They are different colors, that I’ve seen, green, yellow, red, blue. If that seal is broken or torn, notify the gas station attendant.”

Here are a few tips to help you avoid a skimmer when you gas up, from the https://www.consumer.ftc.gov/blog/2018/08/watch-out-card-skimming-gas-pump

Photo credit: National Association of Convenience Stores (NACS) and Conexxus

Photo credit: Royal Canadian Mounted Police in Kamloops, Canada

Try to wiggle the card reader before you put in your card. If it moves, report it to the attendant. Then use a different pump.

If your credit card has been compromised, report it to your bank or card issuer. Federal law limits your liability if your credit, ATM, or debit card is lost or stolen, but your liability may depend on how quickly you report the loss or theft. For more information, read Lost or Stolen Credit, ATM, and Debit Cards.

OVERLAND PARK, Kan. – Feb. 16, 2021 – With extreme cold weather producing historic lows and increased demand, Kansas Gas Service has directed large customers to reduce their usage to ‘plant protection mode’ (lowest possible usage that will keep pipes from freezing and avoid damage to equipment) to prevent outages in Kansas.

“We are planning for potential outages and putting measures in place to keep gas service to our customers and critical facilities,” said Sean Postlethwait, vice president of operations for Kansas Gas Service. “Our large commercial, industrial and transport customers play an important and pivotal role in helping the community avert a disruption in service.”

This curtailment does not apply to schools, hospitals, health care facilities, hotels or lodging facilities, grocery stores, universities, colleges, churches, public safety buildings, multi-family dwellings and apartments.

“Following our regulatory obligations under our curtailment plan, an initial critical step is to take measures to seek assistance from our large commercial and industrial and transport customers to help avoid disruptions,” said Postlethwait.

Customers are encouraged to visit KansasGasService.com/SevereCold for any company severe weather updates.

About Kansas Gas Service

Kansas Gas Service delivers safe, clean and reliable natural gas to more than 639,000 customers in 360 communities in Kansas. We are the largest natural gas distributor in the state, in terms of customers.

We are a division of ONE Gas, Inc. (NYSE: OGS), a stand-alone, 100 percent regulated, publicly traded natural gas utility that trades on the New York Stock Exchange under the symbol “OGS.” ONE Gas is included in the S&P MidCap 400 Index, and is one of the largest natural gas utilities in the United States.

For more information, visit the websites at www.kansasgasservice.com or www.onegas.com

Bourbon County Economic Development Council, Inc. is a not-for-profit started in 1992.

The council “reconstituted” in 2020.

“The bylaws were amended, and the board reconstituted in 2020, to make economic development functions a county-wide effort again, and to reestablish cooperation and trust amongst the disparate geographies in our county,” he said. “We can no longer afford to go it alone, and must work together.”

In the last few months, the council began a search for an economic development director.

Their goal for this month is to hire an economic development director to move the county forward.

“The Human Resource Committee (of BEDCO) is currently running the process of hiring an executive director,” Motley said. “We had 13 applications from all over the United States, and one from overseas.”

Through a qualifications matrix, six applications were selected, and each of the six has completed a test to measure skills and temperament suitable for the job, he said.

The committee will reduce the number of applicants based on their scores, and begin interviewing the finalists soon, Motley said.

Composition of BEDCO

“The board of trustees consists of appointees by the…seven incorporated cities, one each from USD 234, USD 235, Fort Scott Community College, the Fort Scott Area Chamber of Commerce, and two at-large members,” Motley said.

The group is comprised of:

Bourbon County Commissioner Lynne Oharah, City of Fort Scott Commissioner Josh Jones, Jess Ervin representing Uniontown, Mike Blevins-Mapleton, Michael Stewart-Bronson, (Treasurer) Mary Pemberton-Redfield, Misty Adams-Fulton, Ted Hessong-USD234, Bret Howard-USD235, (Vice President) Jim Fewins-Fort Scott Community College,(President) Greg Motley-Fort Scott Area Community Foundation, (At-Large) Mark McCoy and (At-Large) Heather Davis.

“Our goal is to be a trusted vehicle whereby we can act as a catalyst for economic development and any other function that might integrate well on a county-wide basis,” Motley said. “Right now, our most valuable assets are lots in the Fort Scott Industrial Park; in conjunction with the county, we are currently working with an active prospect on a land deal in that vicinity that would bring a new business to town.”

“The main board only meets when there is something of substance to consider,” Motley said.

In addition to the human resource committee, the operations committee is meeting regularly.

Operations Committee

The operations committee met on Feb. 11, and worked on logistics of onboarding the economic development director, including office space, phone, etc., Motley said.

That committee is comprised of Mark McCoy, Lynne Oharah, Mary Pemberton, Misty Adams, and Josh Jones.

“We discussed office locations,” McCoy said. “Cost is number one, we have very limited funds.”

Two locations were discussed: the BWERC ( Bourbon County Workforce and Entrepreneur Resource Center) office above the new Star Emporium Downtown General Store on Main Street and an office inside Landmark Bank, also on Main Street.

“Both of these offer the potential of the first year, no cost,” McCoy said.

Also discussed was the equipment needed for the job.

“Telecommunication is an important part of the job,” McCoy said. “We want to make sure BEDCO has appropriate information technology access.”

The position is being funded by the Bourbon County Commission who committed $130,000 for the total package of salary, benefits, equipment, supplies, transportation expenses, association expenses, and office space, McCoy said.

“The goal is to save taxes in Bourbon County,” McCoy said. “My goal in the future is to have one economic director representing the county.”

Currently, the City of Fort Scott and the Bourbon County Commission both have an economic director.

The city and county recently agreed to share the finance director position, held by Susan Bancroft.

To learn more about this collaboration:

Susan Bancroft Assumes Duties as Bourbon County Business Manager

Name Change

The BEDCO group is considering a name change since they have a new direction of the whole county.

“There are four names under consideration,” McCoy said. “With the new direction, it is important to revise who you are and where you are going.”

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

[Message clipped] View entire message

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Local business owner, Marsha Lancaster, has been in the hospital for over a month, according to her sister Debbie Baxley.

“She went into the hospital at Pittsburg for two to three days, then they took her to Arkansas,” Baxley said.

“Her kidneys were shutting down and they couldn’t find a hospital to take her with COVID (the pandemic virus plaguing the nation and the world),” she said. “They found one in Arkansas and we said just take her to wherever she can get help.”

They have tested Lancaster three times for COVID-19 and each was negative, her sister said.

Lancaster is currently on dialysis every other day and oxygen.

“Her kidneys’ aren’t functioning yet, the doctor said they could kick in any day,” she said. “They have been trying to get her off of oxygen. That’s been going well.”

“We can see her on our cellphone and she looks good when we talk to her,” Baxley said.

Cards can be sent to Marsha at

Regional Springdale NW Medical Center,

609 W. Maple Avenue, 6th floor, attn: Marsha Lancaster

Springdale, Arkansas 72764

Her business is running with the help of others.

Her well-known restaurant, Marsha’s Deli, is continuing with the help of staff and family. The restaurant is located at 6 W. 18th in Fort Scott.

Baxley and her daughter, Shelly Rowe, along with Carla Hemrick, and Lisa Bradley “are taking care of the business for her,” Baxley said.

Monday and Tuesday the restaurant was closed due to the ice roads and arctic weather conditions.

A fundraiser has been started for Lancaster.

Meanwhile, a fundraiser has been started for Lancaster.

“We thought being self-employed, there was no way she wouldn’t need help,” Linda Findley who is spearheading the fundraiser said.

The fundraiser is Friday, Feb. 19 from 11 a.m. to 6 p.m. at the Elk’s Building at 111 W. 19th. People are asked to drive to the east door of the building and orders will be taken by helpers. Then the meals will be brought out to the buyer.

It’s a chicken and noodles dinner with mashed potatoes, green beans, and bread for $10 cash or check only.

Pre-ordering is encouraged. Call 620-215-2036 or 816-797-4884.

Findley said she is anticipating serving 500 meals, with over 200 already ordered.

“Numerous people have sent big donations,” Findley said. “Marrone’s of Pittsburg and G & W Foods of Fort Scott has helped with food.”

Helping the day of the fundraiser will be Nancy Maze, Brenda Collinge, Debbie Myers, JoLynne Mitchell, and Adina Findley, Findley said.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|