Here is a screenshot of the 2005 property taxes for a local business. Half of this amount should have been due on December 20th 2005 and the other half on May 10th 2006. Since the taxes weren’t paid, they should have been published in October 2006 which would have started the redemption period. For non-homestead property that would have been 24 months.

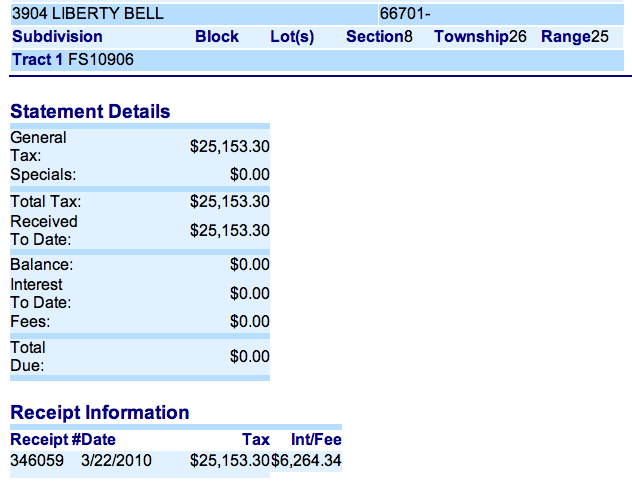

So the property should have been at any Sheriff’s sale that occurred after October of 2008. However, the taxes were not paid until March of 2010. Was there no tax sale from October 2008 until some point after March of 2010? The Bourbon County website lists a 2009 tax sale list, but this property was not included. According to the Commission minutes, there was a tax sale held January 27th, 2010.

When I asked Treasurer wasn’t sure why this property wasn’t on the sale and she didn’t recall any reason why it was held off. It is important to note that there are many stages that property goes through before being listed on a sale and it is entirely possible that it was submitted as property for sale, from the Treasurer’s office but held out based on other criteria.

If there was a reason why the property was held off the tax sale, was the interest calculated correctly? The interest rate for 2005 taxes was 7%. The total amount owed would incurred interest from May 20th 2006 until March 22nd, 2010 or 46 months and two days. Half of the amount would have incurred interest from December 10th, 2005 until May 20th, 2006 or 5 months 10 days. If we round the time to just months the total comes to $7,116.29 in interest. There should have been another $15 or so in fees as well.

According to Susan Porter, who used to work in the Treasurer’s office, the system we are looking at here, has a safe guard against accepting incorrect interest. It requires that you manually over-ride the interest.

When this is entered to actually pay the tax on the tax payment screen the only way for the interest or penalty to be changed or removed is a manual override or to back date the payment calendar date. Until this is done the correct amount of interest and penalties are calculated correctly. ~ Susan Porter source

If this is correct, then someone would have needed to intentionally marked the amount as complete even though the system was showing there was still around $900 owed. I asked the Treasurer the discrepancy could be due to the way that the amortization schedule works. In other words if part of the taxes owed were paid early on, those taxes would no longer be accuring interest. So it is possible the taxes were calculated correctly, but since the date of each payment doesn’t show up on the public website, it is hard to tell.

Interestingly this particular company does have a payment plan that was setup in 2010. They own just under $30,000. The payment plan states that they will pay $2,000 per month from April 20, 2011 until May 20, 2012. This only comes to $28,000 which is about $2,000 less than what they owe without factoring in the interest.

According to Mr. Sercer, he was told that the payment plans were based on an amortization schedule produced by the old computer system and that sometimes it came up with “crazy” interest rates. The Treasurer confirmed that this was likely what had happened in this situation. It seems very odd that it would generate a completely even number that doesn’t even add up to the full amount much less include interest.

The problem isn’t so much that the property wasn’t sold. Obviously it is better if the taxes are paid. However, if a property doesn’t have the threat of being sold, it is possible for other payments to become the priority.

Is it possible that simply following the timelines specified for selling delinquent property would have encouraged enough payments to have made the past mill levy increase unnecessary?